Auto Insurance Premiums Are Up. So Why Are Insurers Still Losing Money?

Albertans have a strange relationship with auto insurance.

We notice the price, we compare it to other provinces, and we assume that if premiums rise, insurers must be doing just fine.

But the numbers tell a messier story: premiums can rise while the auto insurance business is still unprofitable. Not because of vibes. Because of math.

The headline numbers (the “wait, what?” section)

Recent Alberta market data shows:

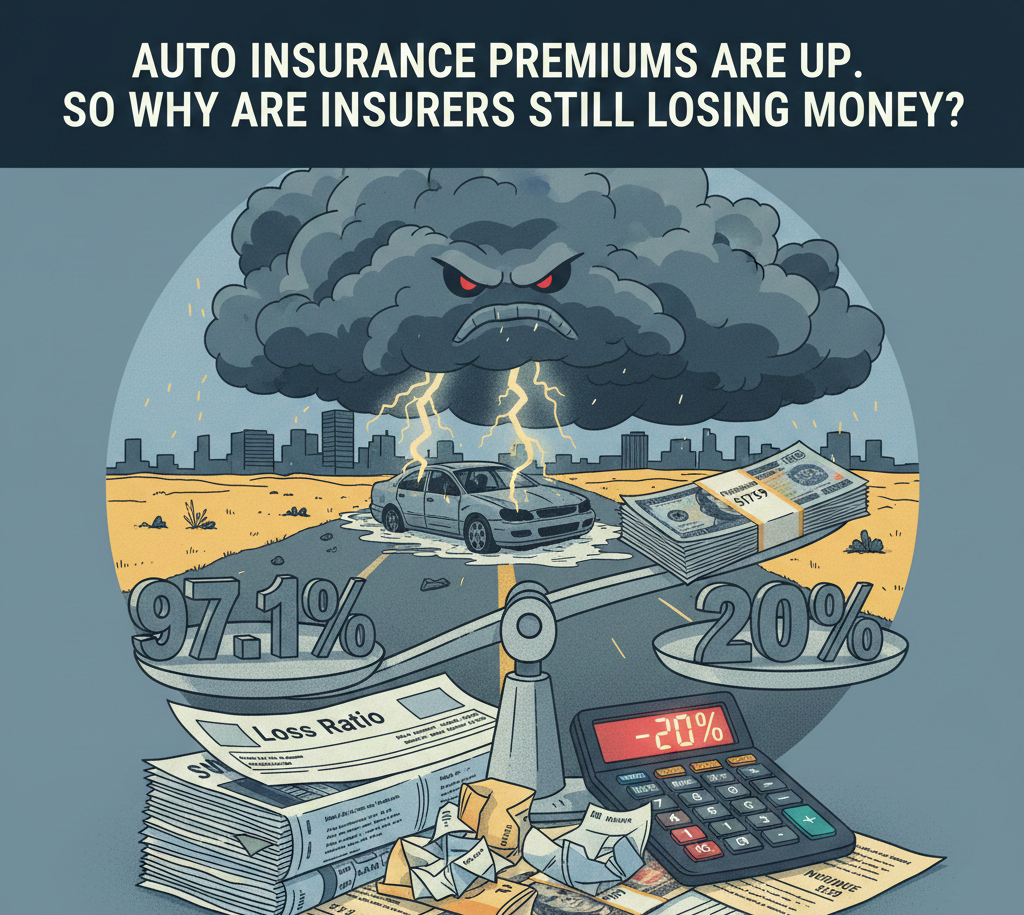

The average written premium rose 5.5% to $1,759 (from $1,668).

The auto loss ratio was 97.1%.

If you’re not living in insurance spreadsheets all day, here’s the translation:

For every $1.00 collected in premium, insurers paid about $0.97 in claims… before paying the costs of running the business (broker compensation, staffing, technology, claims handling, overhead, reinsurance, and so on).

And those expenses don’t come for free. A common industry ballpark for the expense ratio is around the high-20% range. Stack that on top of a 97% loss ratio, and you don’t get “slightly less profitable.” You get structurally underwater.

“But my premium went up…”

Yep. And you’re not imagining it.

Premiums are moving upward because claim costs are moving upward faster. Alberta’s auto insurance system is currently dealing with several cost drivers at the same time, and they don’t politely take turns.

1) Bodily injury severity is doing the heavy damage

Bodily injury severity has increased dramatically in recent years. One published Alberta trend showed bodily injury severity up 96.2% from 2020–2024, including 11.1% in the most recent year.

Frequency can stabilize, but when severity keeps climbing, the whole system pays more for the same number of incidents.

2) Catastrophe losses are no longer “rare”

Weather is now a recurring line item, not an exception. The August 2024 Calgary hailstorm is a perfect example: $2.8 billion in insured damage. In some neighborhoods, comprehensive loss ratios reportedly went north of 800%.

That’s not a “bad quarter.” That’s a single event that changes how insurers think about pricing, deductibles, and appetite.

3) Rate controls can smooth today and sharpen tomorrow

When rate movement is constrained (especially for certain driver segments), insurers can’t always make gradual adjustments that match rising claim costs. The result is often a pressure-cooker effect: the market tries to catch up later, and it can feel like renewals jump more abruptly than anyone wants.

This is one reason consumers sometimes experience the frustrating combo of:

higher premiums, and

tighter underwriting, and

fewer “nice-to-have” coverages being offered

All at the same time.

So… how unprofitable are we talking?

In the most recently published Alberta results, the overall return on premium (a profitability measure) was reported at approximately -20% for the accident year being summarized.

In normal-person language: the industry, overall, isn’t just “making less.” It’s losing money in a way that forces change.

And it’s not evenly bad. Some insurers lose more, some lose less, and a small handful may still manage to stay above water depending on portfolio mix, claims outcomes, and underwriting discipline.

When the market looks like this, insurers don’t respond by saying, “No worries, let’s keep everything broad and flexible.”

They respond like insurers respond in every hard market:

tightening underwriting rules

reducing appetite for certain vehicles/territories/driver profiles

limiting optional coverages

increasing deductibles or restricting physical damage on certain risks

getting pickier at renewal

Which is exactly what brokers and clients have been seeing.

Why this matters to you (even if you never file a claim)

Because your premium isn’t only about your personal driving record.

It’s also shaped by:

the cost to repair modern vehicles (more sensors, more calibration, pricier parts)

medical and treatment costs

how claims are handled and litigated in the broader system

catastrophe frequency and severity

how much uncertainty insurers need to price for just to keep capacity in the province

You can be a perfect driver and still live in a system that’s getting more expensive to operate.

The forward-looking part: what changes next?

Alberta is moving toward a Care-First approach starting in 2027, with the goal of reducing legal friction, improving access to care, and making costs more predictable.

Whether that creates real affordability will come down to the details: benefit levels, treatment pathways, dispute resolution, and whether the system actually reduces the expensive parts of claims rather than simply rearranging them.

But here’s the practical takeaway for 2025–2026:

If bodily injury severity stays hot and catastrophe losses keep arriving like unwanted group texts, the market will keep trying to find oxygen. And it usually finds oxygen in two places:

pricing, and

restricting availability (underwriting appetite and coverage options)

Bottom line

Premiums are up. But the underlying profitability math in Alberta auto has been strained.

Average premium: $1,759 (up 5.5%)

Loss ratio: 97.1%

Profitability measure reported around: -20% (for the accident year summarized)

That combination explains why it can feel like you’re paying more and getting less flexibility at the same time.